As the Euro Turns 20, a Look Back at Who Fared the Best. And Worst.

Mario Draghi, president of the European Central Bank, once likened the euro to a bumblebee—a “mystery of nature” that shouldn’t be able to fly, but somehow does.

Draghi used this metaphor at the height of the tumultuous Greek debt crisis in 2012, when many wondered if the demise of Europe’s single currency was imminent.

Now, two decades after its birth, the euro has taken flight and, by some measures, has even soared. Membership has grown to 19 countries from the original 11, and the size of the euro-area economy has swelled by 72 percent to 11.2 trillion euros ($12.8 trillion), second only to that of the U.S. and positioning the European Union as a global force to be reckoned with.

A Global Player

This achievement masks divergences that were perhaps impossible to avoid for a region of such enormous economic and cultural diversity. When European nations traded in the power to set their own interest rates and submitted to the bloc’s fiscal limits, they were counting on greater economic welfare to follow. Bloomberg created a series of tests for the euro’s 20th anniversary to see how they did. The results, outlined in illustrations below, show only a handful are clearly flourishing.

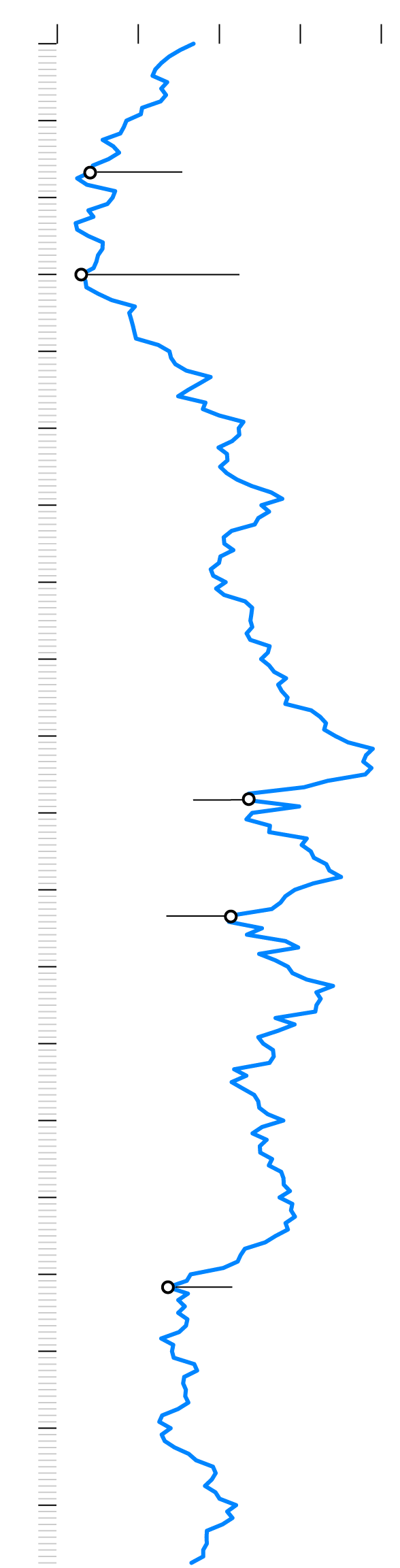

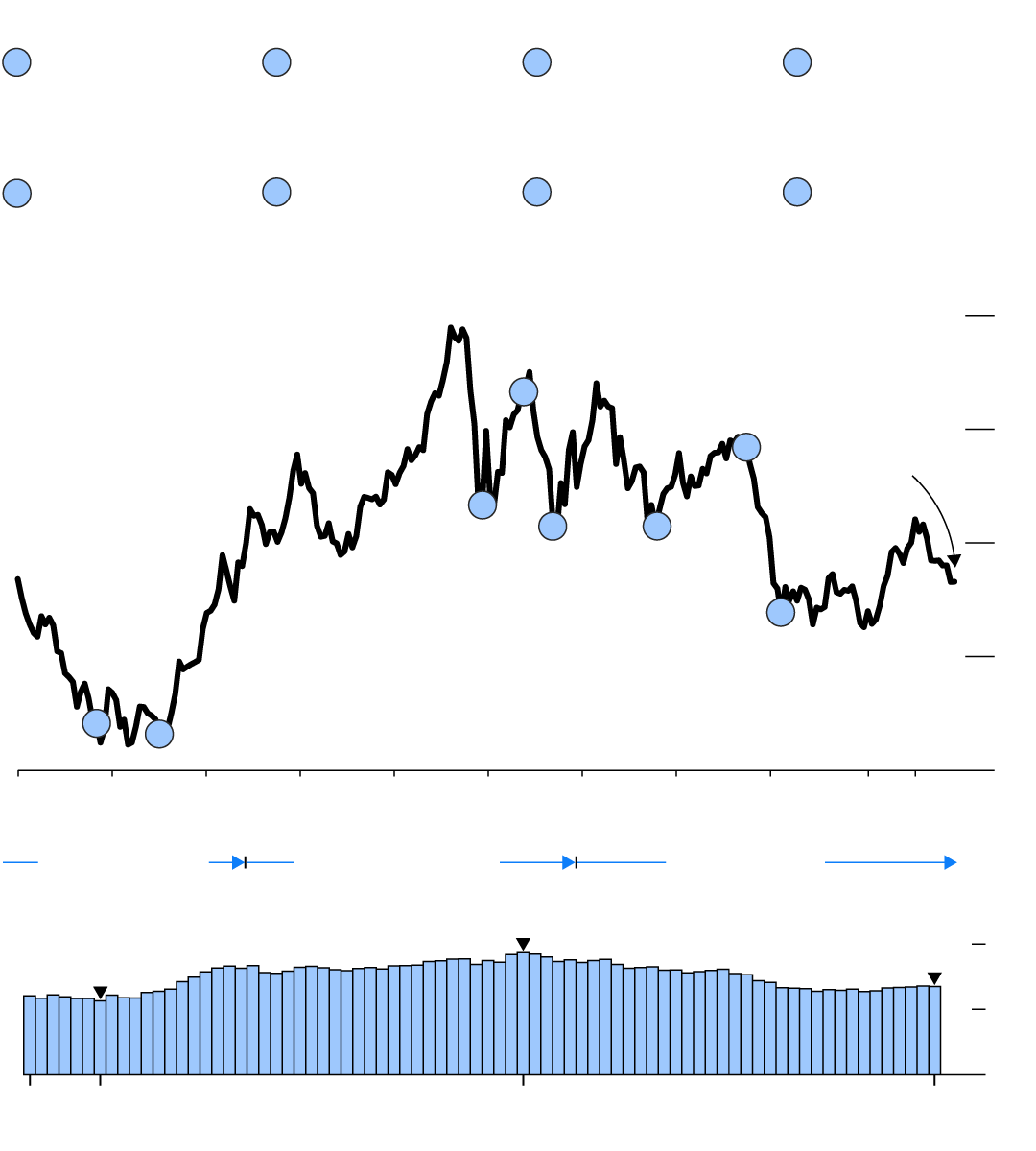

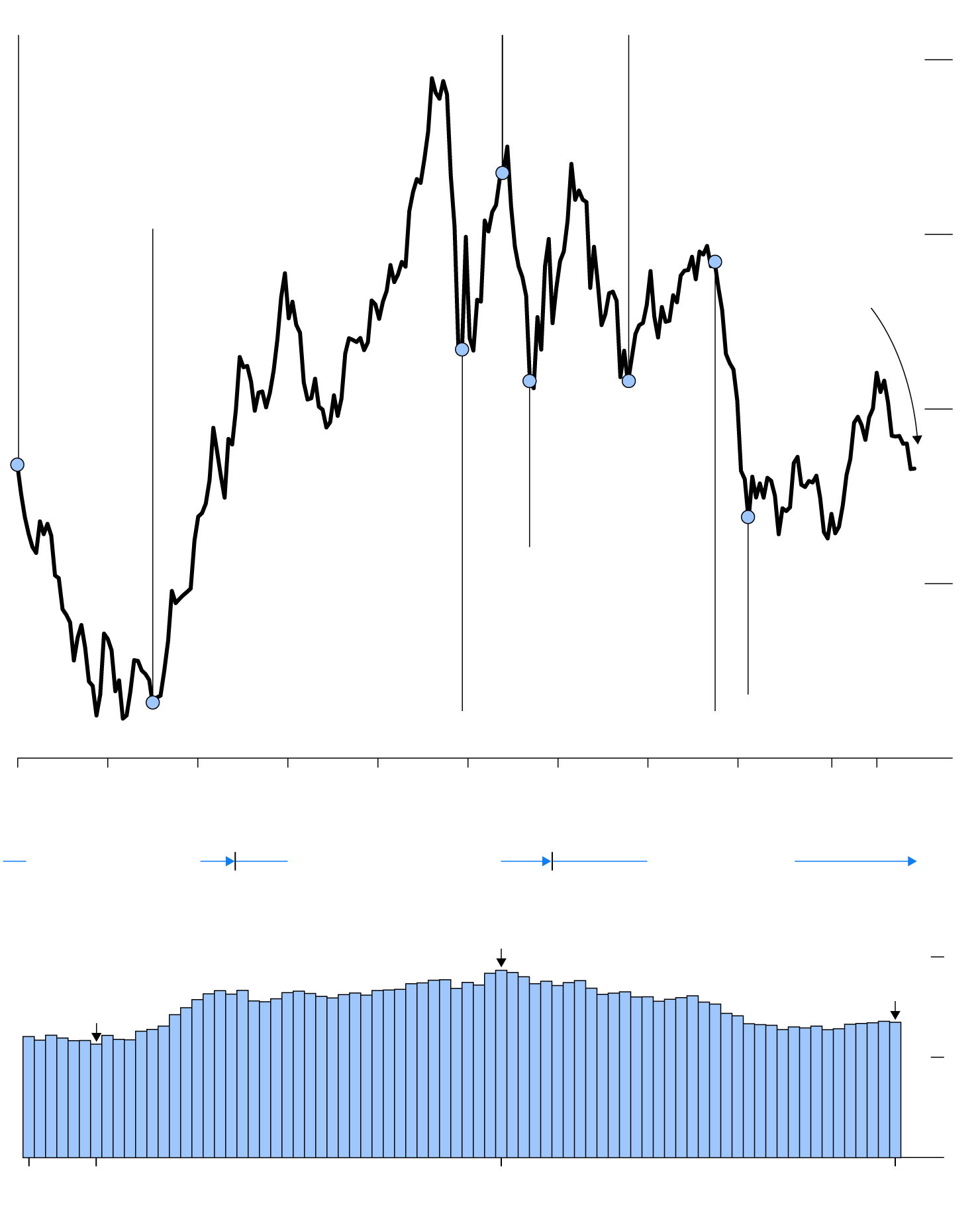

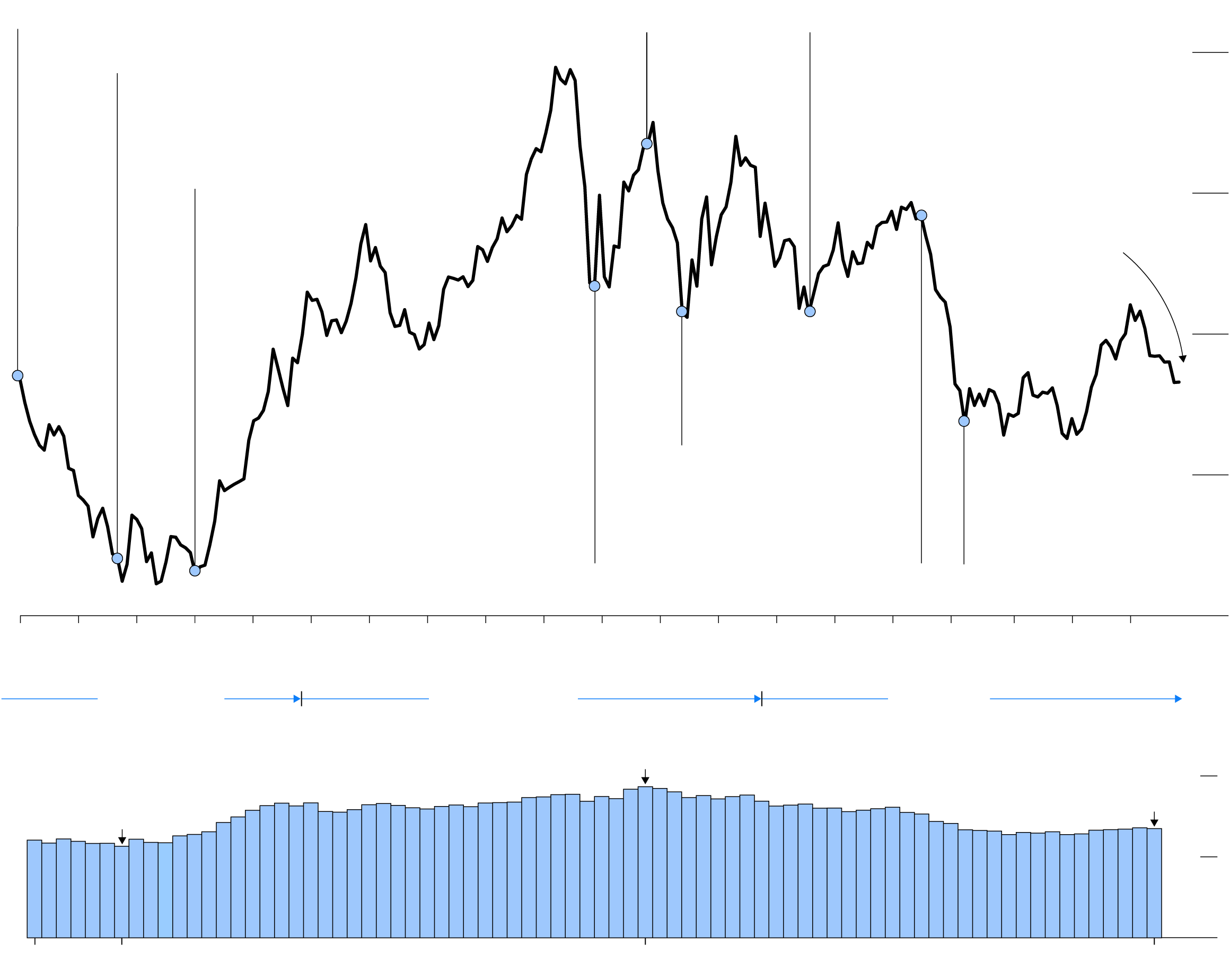

The euro has swung wildly since its debut on Jan. 1, 1999, three years before notes and coins went into circulation. It’s been especially turbulent this decade as bailouts of debt-laden members and a double-dip recession nearly tore the monetary union apart. By flooding the bloc with cash, Draghi managed to keep Europe’s currency dream alive. That didn’t reverse the damage to the euro’s reputation, though; its share of global reserves is down nearly 30 percent since a 2009 peak.

Turbulent Ride

1.20

1.40

1.60

0.80

1.00

’99

Sep. 2000

€1 = $0.88

The ECB and other central banks intervene to prop up the euro

’00

’01

Jan. 2002

0.86

Euro banknotes start circulating

’02

’03

’04

’05

’06

’07

’08

Nov. 2008

1.27

Data confirms euro area is in its first recession

’09

’10

May 2010

1.23

Greece becomes first of five euro-area countries to be bailed out*

’11

’12

’13

’14

’15

March 2015

1.07

ECB quantitative easing (QE) program begins

’16

’17

’18

Price of one euro in U.S. dollars

Sep. 2000 |

€1 = $0.88

The ECB and other central banks intervene to prop up the euro

Jan. 2002 | 0.86

Euro banknotes start circulating

Nov. 2008 | 1.27

Data confirms euro area is in its first recession

Oct. 2009 | 1.47

Greece kicks off multi-year European debt crisis

1

4

2

3

July 2012 | 1.23

ECB President Mario Draghi vows to do “whatever it takes” to safeguard the euro

June 2014 | 1.37

ECB becomes first major central bank to cut interest rates below zero

March 2015 | 1.07

ECB quantitative easing (QE) program begins

May 2010 | 1.23

Greece becomes first of five euro-area countries to be bailed out*

6

7

8

5

$1.60

4

1.40

Dec. 2018

ECB halts QE

7

3

1.20

6

5

8

1.00

1

2

0.80

’99

’13

’18

’05

’09

’11

’17

’01

’03

’07

’15

European Central Bank Presidents

Wim Duisenberg

Jean-Claude Trichet

Mario Draghi

High

28.02

Percent share of global reserves

30%

low

16.97

20.26

15

0

Sept.

2009

March

1999

Sept.

2000

June

2018

Price of one euro in U.S. dollars

Oct. 2009

1.47

Greece kicks off multi-year European debt crisis

July 2012

1.23

ECB President Mario Draghi vows to do “whatever it takes” to safeguard the euro

Jan. 1999

€1 = $1.14

Euro debuts

$1.60

1.40

Jan. 2002

0.86

Euro banknotes start circulating

Dec. 2018

ECB halts QE

1.20

May 2010

1.23

Greece becomes first of five euro area countries to be bailed out*

1.00

June 2014

1.37

ECB becomes first major central bank to cut interest rates below zero

Nov. 2008

1.27

Data confirms euro area is in its first recession

March 2015

1.07

ECB quantitative easing (QE) program begins

0.80

’05

’09

’13

’99

’01

’03

’07

’11

’15

’17

’18

European Central Bank Presidents

Wim Duisenberg

Jean-Claude Trichet

Mario Draghi

High

28.02

Percent share of global reserves

30%

20.26

low

16.97

15

0

Sept.

2009

March

1999

Sept.

2000

June

2018

Price of one euro in U.S. dollars

Jan. 1999

€1 = $1.14

Euro debuts

Oct. 2009

1.47

Greece kicks off multi-year European debt crisis

July 2012

1.23

ECB President Mario Draghi vows to do “whatever it takes” to safeguard the euro

$1.60

Sep. 2000

0.88

The ECB and other central banks intervene to prop up the euro

1.40

Jan. 2002

0.86

Euro banknotes start circulating

Dec. 2018

ECB halts QE

1.20

May 2010

1.23

Greece becomes first of five euro-area countries to be bailed out*

1.00

June 2014

1.37

ECB becomes first major central bank to cut interest rates below zero

March 2015

1.07

ECB quantitative easing (QE) program begins

Nov. 2008

1.27

Data confirms euro area is in its first recession

0.80

’99

’00

’01

’02

’03

’04

’05

’06

’07

’08

’09

’10

’11

’12

’13

’14

’15

’16

’17

’18

European Central Bank Presidents

Wim Duisenberg

Jean-Claude Trichet

Mario Draghi

High

28.02

Percent share of global reserves

30%

20.26

low

16.97

15

0

March

1999

Sept.

2000

Sept.

2009

June

2018

Exam Time

To take stock of the project so far, Bloomberg Economics ran euro-area countries through 10 economic tests to capture the extent to which member states reaped the benefits of greater stability and economic integration, as well as their capacity to remain competitive and stabilize their economies during the euro-area sovereign debt crisis.

The tests don’t show whether member states would have been better off outside of the euro, nor do they measure overall prosperity and economic health. Rather, they illustrate how well each country seized the opportunities and navigated the risks associated with sharing a currency.

The results portray a divided continent. Of the 16 countries tested, six ended up with As, five got Bs and another handful scored Cs. The three Baltic nations that joined since 2011 weren’t tested because they haven’t been in the group long enough.

Report Card

Each indicator was designed so that a positive response received an A grade, a neutral response a B grade and a negative response a C grade. Some criteria only applied to the initial 12 members, and so were left blank for later adopters. For full details, see the methodology at the bottom. A country’s overall score was determined based on how many more As it achieved than Cs, like this:

- A 2 or more, very good

- B 0 to 1, satisfactory

- C -1 or less, mediocre

Very Good Grades

It’s no surprise that Germany aced the tests—the euro was tantamount to devaluation for Europe’s largest economy, and thus a boon for trade and competitiveness. Late joiners Slovakia and Slovenia were also among the top achievers, largely because the euro drastically reduced exchange-rate risks, enabling them to deepen trade relations in the bloc.

What Our Economist Says: “Key to the success of these countries was the development of deeply integrated production networks across the euro area, but even more so, their ability to keep labor costs under check and improve their competitiveness through the first decade, often through structural reforms. Entering the downturn from a stronger position, they were also better-placed to weather the euro crisis.” —Maeva Cousin, Bloomberg Economics

Report Cards: Top of the Class

Satisfactory Grades

The benefits of monetary union weren’t quite so pronounced for some founding members. While the countries in this category mostly remained externally competitive, when hard times hit, Ireland and Portugal in particular struggled because they didn’t have enough room to maneuver with fiscal policy alone and flirted with deflation. While Greece suffered mightily during the sovereign debt crisis, it also eked out a B. For all that went wrong, being part of the euro for 18 years made it possible for Greece to build new trade relationships with Europe’s wealthier core. Transferring monetary policy to a credible central bank brought greater price stability in the early years and the recent past has seen a big improvement in competitiveness.

Report Cards: Middle of the Class

Mediocre Grades

The worst marks went to three of Europe’s five largest economies: France, Italy and Spain. They suffered substantially from losing the ability to devalue when responding to crises, in particular because they had limited room to lower wages so their competitiveness deteriorated. Even in the pre-crisis years, the three nations failed to capitalize on the currency union by deepening trading relationships in the bloc—and only Spain has begun to change this since.

What Our Economist Says: “These countries generally enjoyed a mixed blessing upon joining the euro. First, greater credibility led to substantial easing in their financial conditions. Growth soared, but without sufficient structural reforms, their economies overheated and competitiveness deteriorated. The crisis then led to a brutal adjustment and threw into light the lack of fiscal capacity, at the country and at the euro-area level, to soften the impact of shocks.” —Maeva Cousin, Bloomberg Economics

Report Cards: Bottom of the Class

Next Test

Beyond the economic disparities, there’s something that matters even more for the euro’s future: how Europeans feel about it. The single currency was always part of a broader political project to ensure peaceful coexistence in Europe, bringing people and countries closer together following two world wars.

The sovereign debt crisis, the rise of populist radical-right parties and Britain’s vote to leave the EU have tested that cohesion. Polls show popular support for the euro has plunged in Italy, which recently elected an anti-establishment government that spent several months warring with the European Commission over its budget.

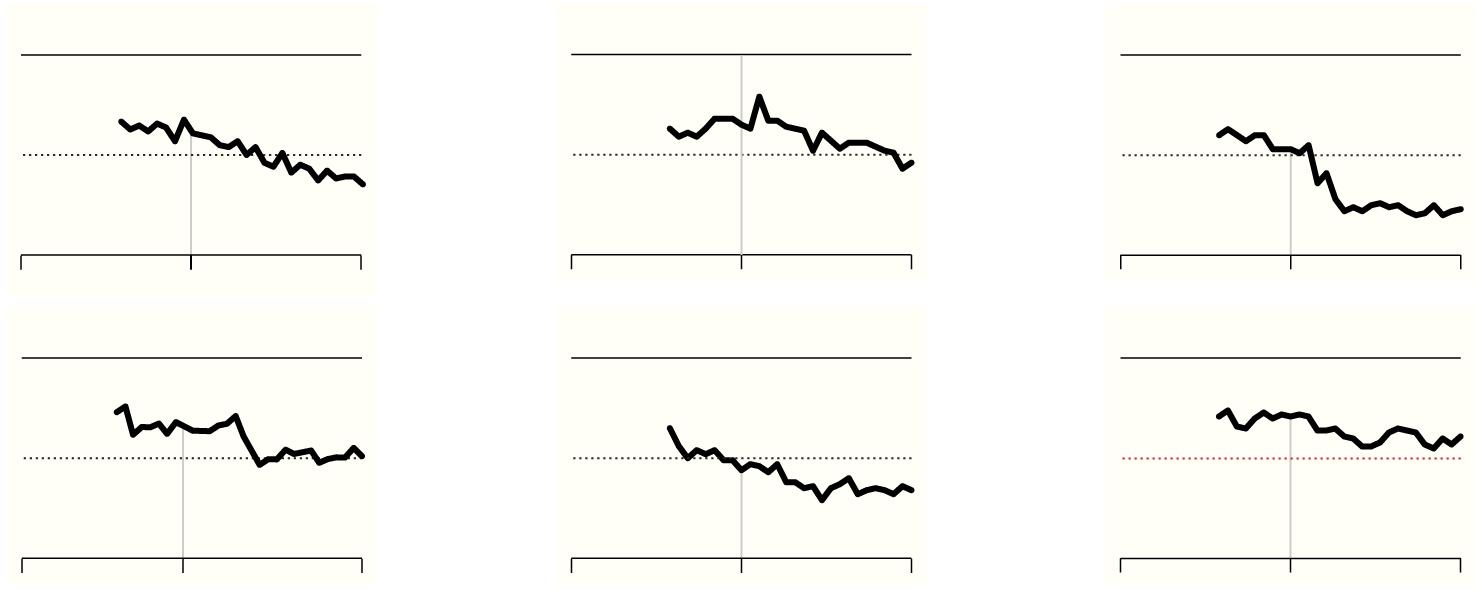

Yet in nations that use the euro, most people are still overwhelmingly fans. Sentiment has improved in 13 member states since they joined, with double-digit bumps in Austria, Finland, Germany and Portugal. Even in Italy, which witnessed a roughly 25-point decline, around 60 percent of people favor sharing a currency with their neighbors.

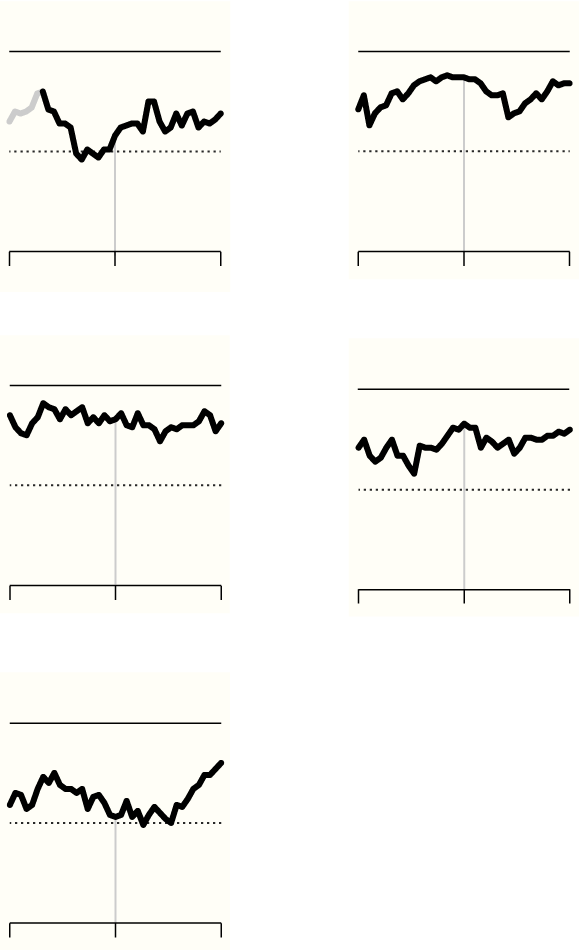

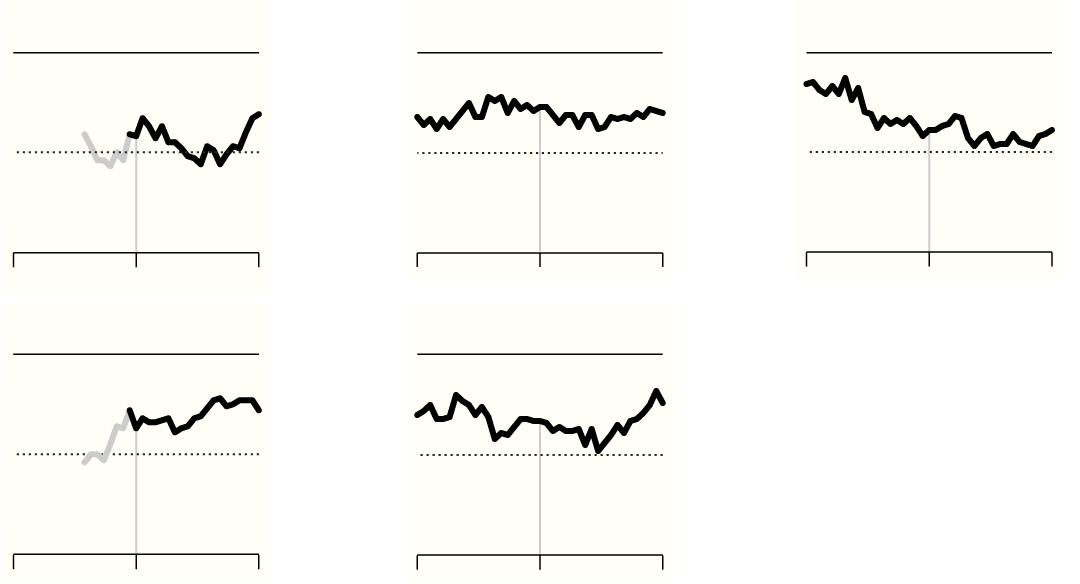

Happy People

Austria

Belgium

100%

50

Recession

0

’99

’18

Finland

Germany

Slovakia

Slovenia

Adopts euro

Austria

Belgium

Finland

100%

50

Recession

0

’99

’18

Germany

Slovakia

Slovenia

Adopts euro

Belgium

Austria

Finland

100%

50

Recession

0

’99

’18

Slovakia

Slovenia

Germany

Adopts euro

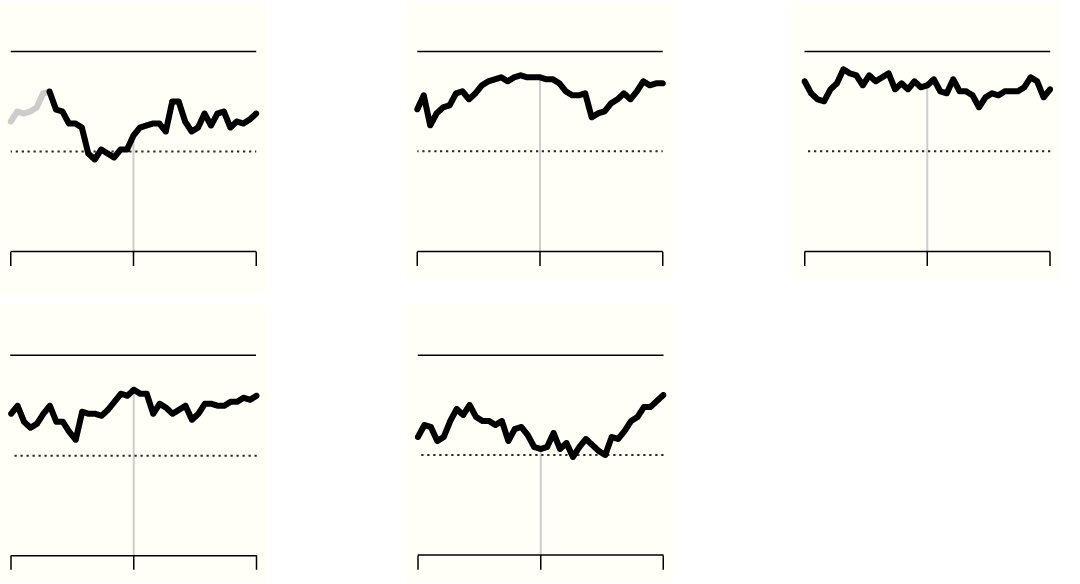

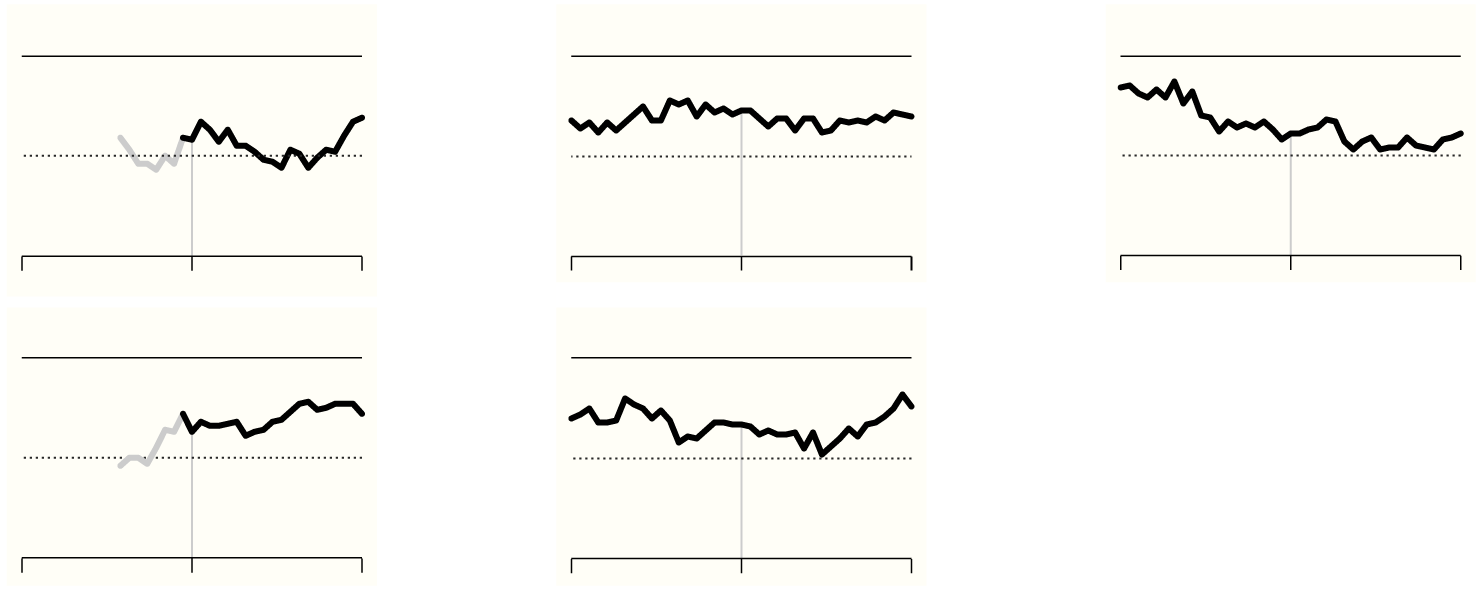

Popular Currency

Greece

Ireland

100%

50

0

’99

’18

Luxembourg

Netherlands

Portugal

Greece

Ireland

Luxembourg

100%

50

0

’99

’18

Netherlands

Portugal

Greece

Ireland

Luxembourg

100%

50

0

’99

’18

Netherlands

Portugal

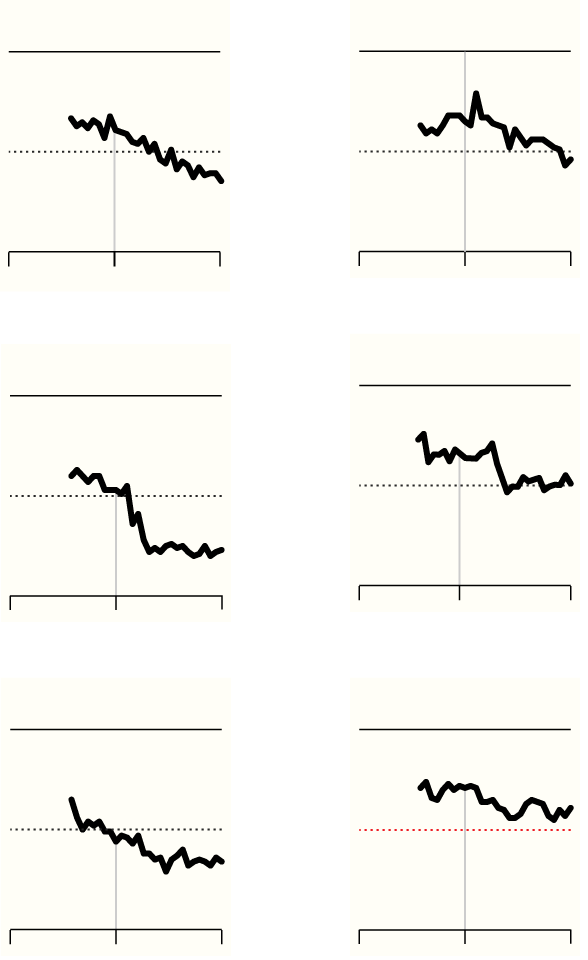

Better Together

Cyprus

France

100%

50

0

’99

’18

Italy

Malta

Spain

Cyprus

Italy

France

100%

50

0

’99

’18

Spain

Malta

Cyprus

Italy

France

100%

50

0

’99

’18

Spain

Malta

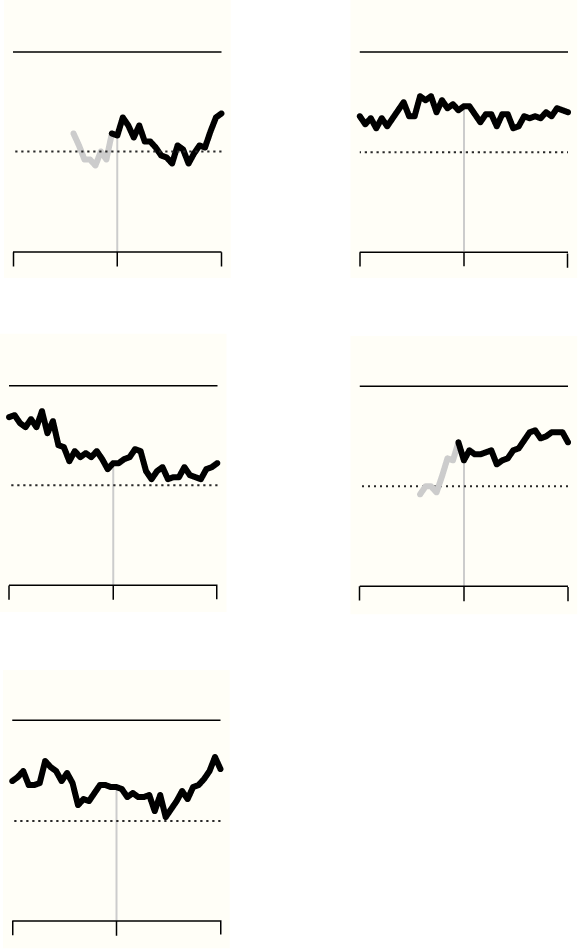

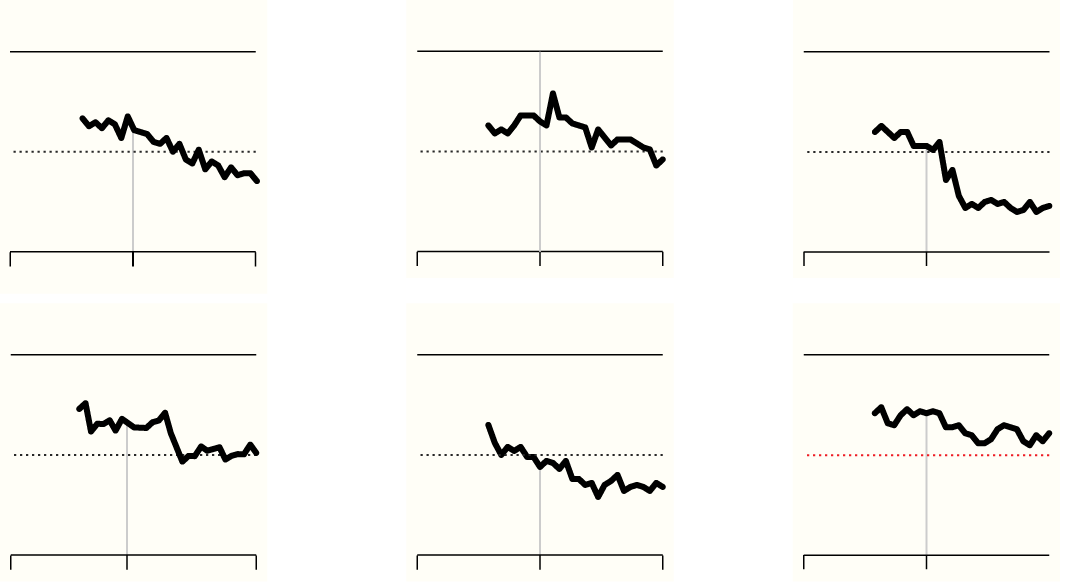

That’s not to say everyone is queuing to join. Polls conducted since 2012 show only 35 percent of Poles and 23 percent of Czechs, on average, are eager to sign up. They, like many Hungarians, are loath to give up their national currencies, even though the EU’s Maastricht Treaty technically requires them to. Among countries eligible for membership, only in Romania does support surpass 60 percent.

Not So Keen

Bulgaria

Croatia

100%

50

0

’99

’18

Hungary

Czech Rep

Poland

Romania

Bulgaria

Croatia

Czech Republic

100%

50

0

’99

’18

Hungary

Poland

Romania

Bulgaria

Croatia

Czech Republic

100%

50

0

’99

’18

Hungary

Poland

Romania

For its next decade, then, the euro’s success will hinge a lot on its ability to carry on defying the economic and political odds stacked against it, and keep flying anyways.